Consolidated Financial Statements 2015

Consolidated Financial Statements 2015

of the Volksbanken Raiffeisenbanken Cooperative Financial Network

Income statement for the period January 1 to December 31, 2015

| Note no. | 2015 € million | 2014 € million | Change (percent) | |

|---|---|---|---|---|

| Net interest income | 2. | 20,021 | 20,047 | –0.1 |

| Interest income and current income and expense | 30,657 | 31,822 | –3.7 | |

| Interest expense | –8,771 | –10,610 | –17.3 | |

| Allowances for losses on loans and advances | 3. | –74 | –299 | –75.3 |

| Net fee and commission income | 4. | 5,798 | 5,467 | 6.1 |

| Fee and commission income | 7,292 | 6,793 | 7.3 | |

| Fee and commission expense | –1,494 | –1,326 | 12.7 | |

| Gains and losses on trading activities | 5. | 607 | 752 | –19.3 |

| Gains and losses on investments | 6. | –561 | 148 | >100.0 |

| Other gains and losses on valuation of financial instruments | 7. | 363 | 435 | –16.6 |

| Premiums earned | 8. | 14,418 | 13,927 | 3.5 |

| Gains and losses on investments held by insurance companies and other insurance company gains and losses | 9. | 3,013 | 4,388 | –31.3 |

| Insurance benefit payments | 10. | –14,664 | –15,264 | –3,9 |

| Insurance business operating expenses | 11. | –1,774 | –1,770 | 0.2 |

| Administrative expenses | 12. | –17,234 | –16,895 | 2.0 |

| Other net operating expense/income | 13. | –126 | –281 | –55.2 |

| Profit before taxes | 9,787 | 10,655 | –8.1 | |

| Income taxes | 14. | –2,820 | –2,848 | –1,0 |

| Net profit | 6,967 | 7,807 | –10.8 | |

Attributable to: | ||||

| Shareholders of the Cooperative Financial Network | 6,761 | 7,555 | –10.5 | |

| Non-controlling interests | 206 | 252 | –18.3 |

Statement of comprehensive income for the period January 1 to December 31, 2015

| 2015 € million | 2014 € million | Change (percent) | |

|---|---|---|---|

| Net profit | 6,967 | 7,807 | –10.8 |

| Other comprehensive income/loss | 854 | –513 | >100,0 |

| Items that may be reclassified to the income statement | 219 | 956 | –77.1 |

| Gains and losses on available-for-sale financial assets | 103 | 1,397 | –92.6 |

| Gains and losses on cash flow hedges | 14 | –31 | >100.0 |

| Exchange differences on currency translation of foreign operations | 44 | 12 | >100.0 |

| Gains and losses on hedges of net investments in foreign operations | –24 | –16 | 50.0 |

| Share of other comprehensive income/loss of joint ventures and associates accounted for using the equity method | 17 | 27 | –37.0 |

| Income taxes relating to components of other comprehensive income/loss | 65 | –433 | >100.0 |

| Items that cannot be reclassified to the income statement | 635 | –1,469 | >100.0 |

| Gains and losses arising from remeasurements of defined benefit plans | 905 | –2,092 | >100,0 |

| Share of other comprehensive income/loss of joint ventures and associates accounted for using the equity method | –1 | –4 | –75.0 |

| Income taxes relating to components of other comprehensive income/loss | –269 | 627 | >100,0 |

| Total comprehensive income | 7,821 | 7,294 | 7.2 |

Attributable to: | |||

| Shareholders of the Cooperative Financial Network | 7,589 | 6,950 | 9.2 |

| Non-controlling interests | 232 | 344 | –32.6 |

Balance sheet as at December 31, 2015

| Assets | Note no. | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|---|

| Cash and cash equivalents | 15. | 20,536 | 15,656 | 31,2 |

| Loans and advances to banks | 16. | 32,988 | 38,293 | –13,9 |

| Loans and advances to customers | 16. | 700,608 | 670,683 | 4,5 |

| Allowances for losses on loans and advances | 17. | –7,631 | –8,519 | –10,4 |

| Derivatives used for hedging (positive fair values) | 18. | 1,050 | 1,099 | –4,5 |

| Financial assets held for trading | 19. | 53,570 | 61,181 | –12,4 |

| Investments | 20. | 249,960 | 249,219 | 0,3 |

| Investments held by insurance companies | 21. | 82,766 | 77,545 | 6,7 |

| Property, plant and equipment, and investment property | 22. | 11,168 | 11,429 | –2,3 |

| Income tax assets | 23. | 3,772 | 4,484 | –15,9 |

| Other assets | 24. | 13,732 | 14,690 | –6,5 |

| Total assets | 1,162,519 | 1,135,760 | 2,4 |

| Equity and liabilities | Note no. | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|---|

| Deposits from banks | 25. | 99,505 | 103,526 | –3,9 |

| Deposits from customers | 25. | 739,218 | 713,485 | 3,6 |

| Debt certificates including bonds | 26. | 70,248 | 66,981 | 4,9 |

| Derivatives used for hedging (negative fair values) | 18. | 9,453 | 10,423 | –9,3 |

| Financial liabilities held for trading | 27. | 45,397 | 52,760 | –14,0 |

| Provisions | 28. | 12,563 | 13,661 | –8,0 |

| Insurance liabilities | 29. | 78,929 | 74,670 | 5,7 |

| Income tax liabilities | 23. | 1,263 | 1,198 | 5,4 |

| Other liabilities | 30. | 7,569 | 7,819 | –3,2 |

| Subordinated capital | 31. | 5,367 | 4,736 | 13,3 |

| Equity | 93,007 | 86,501 | 7,5 | |

| Equity of the Cooperative Financial Network | 90,088 | 83,153 | 8,3 | |

| Subscribed capital | 10,922 | 10,762 | 1,5 | |

| Capital reserves | 784 | 754 | 4,0 | |

| Retained earnings | 70,122 | 62,807 | 11,6 | |

| Revaluation reserve | 1,444 | 1,258 | 14,8 | |

| Cash flow hedge reserve | –7 | –15 | –53,3 | |

| Currency translation reserve | 62 | 32 | 93,8 | |

| Unappropriated earnings | 6,761 | 7,555 | –10,5 | |

| Non-controlling interests | 2,919 | 3,348 | –12,8 | |

| Total equity and liabilities | 1,162,519 | 1,135,760 | 2,4 |

Statement of changes in equity

€ million

| Subscribed capital | Capital reserves | Equity earned by the Cooperative Financial Network | Revaluation reserve | Cash flow hedge reserve | Currency translation reserve | Equity of the Cooperative Financial Network | Non-controlling interests | Total equity | |

|---|---|---|---|---|---|---|---|---|---|

| Equity as at Jan. 1, 2014 | 10,424 | 708 | 64,683 | 435 | 4 | 12 | 76,266 | 3,120 | 79,386 |

| Net profit | – | – | 7,555 | – | – | – | 7,555 | 252 | 7,807 |

| Other comprehensive income/loss | – | – | –1,441 | 835 | –19 | 20 | –605 | 92 | –513 |

| Total comprehensive income | – | – | 6,114 | 835 | –19 | 20 | 6,950 | 344 | 7,294 |

| Issue and repayment of equity | 338 | 46 | – | – | – | – | 384 | 144 | 528 |

| Changes in the scope of consolidation | – | – | 46 | –12 | – | – | 34 | 1 | 35 |

| Acquisition/disposal of non-controlling interests | – | – | 101 | – | – | – | 101 | –198 | –97 |

| Dividends paid | – | – | –582 | – | – | – | –582 | –63 | –645 |

| Equity as at Dec. 31, 2014 | 10,762 | 754 | 70,362 | 1,258 | –15 | 32 | 83,153 | 3,348 | 86,501 |

| Net profit | – | – | 6,761 | – | – | – | 6,761 | 206 | 6,967 |

| Other comprehensive income/loss | – | – | 627 | 163 | 8 | 30 | 828 | 26 | 854 |

| Total comprehensive income | – | – | 7,388 | 163 | 8 | 30 | 7,589 | 232 | 7,821 |

| Issue and repayment of equity | 160 | 30 | – | – | – | – | 190 | –248 | –58 |

| Changes in the scope of consolidation | – | – | 4 | – | – | – | 4 | 1 | 5 |

| Acquisition/disposal of non-controlling interests | – | – | –304 | 23 | – | – | –281 | –351 | –632 |

| Dividends paid | – | – | –567 | – | – | – | –567 | –63 | –630 |

| Equity as at Dec. 31, 2015 | 10,922 | 784 | 76,883 | 1,444 | –7 | 62 | 90,088 | 2,919 | 93,007 |

| Breakdown of subscribed capital: | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Cooperative shares | 10,673 | 10,271 | 3.9 |

| Share capital | 144 | 176 | –18.2 |

| Capital of silent partners | 105 | 315 | –66.7 |

| Total | 10,922 | 10,762 | 1.5 |

Statement of cash flows

| 2015 € million | 2014 € million | |

|---|---|---|

| Net profit | 6,967 | 7,807 |

| Non-cash items included in net profit and reconciliation to cash flows from operating activities | ||

| Depreciation, impairment losses, and reversal of impairment losses on assets, and other non-cash changes in financial assets and liabilities | 451 | –1,676 |

| Non-cash changes in provisions | –1,102 | 2,305 |

| Changes in insurance liabilities | 7,262 | 9,977 |

| Other non-cash income and expenses | 366 | 981 |

| Gains and losses on the disposal of assets and liabilities | 476 | –152 |

| Other adjustments (net) | –18,213 | –18,746 |

| Subtotal | –3,793 | 496 |

| Cash changes in assets and liabilities arising from operating activities | ||

| Loans and advances to banks and customers | –26,402 | –27,134 |

| Other assets from operating activities | 350 | 1,075 |

| Derivatives used for hedging (positive and negative fair values) | –835 | 434 |

| Financial assets and financial liabilities held for trading | –748 | 4,812 |

| Deposits from banks and customers | 21,475 | 26,543 |

| Debt certificates including bonds | 3,132 | –909 |

| Other liabilities from operating activities | –3,145 | –2,676 |

| Interest, dividends and operating lease payments received | 31,997 | 29,063 |

| Interest paid | –7,153 | –8,333 |

| Income taxes paid | –1,897 | –2,314 |

| Cash flows from operating activities | 12,981 | 21,057 |

| Proceeds from the sale of investments | 6,742 | 13,551 |

| Proceeds from the sale of investments held by insurance companies | 18,764 | 24,670 |

| Proceeds from the sale of intangible non-current assets | 159 | 18 |

| Payments for acquisitions of investments | –8,625 | –23,490 |

| Payments for acquisitions of investments held by insurance companies | –23,673 | –32,110 |

The consolidated statement of cash flows shows the changes in cash and cash equivalents during the financial year. Cash and cash equivalents consist of cash on hand, balances with central banks and other government institutions as well as treasury bills and non-interest bearing treasury notes. The cash and cash equivalents do not include any financial investments with a maturity of more than three months at the date of acquisition. Changes in cash and cash equivalents are broken down into operating, investing and financing activities.

| 2015 € million | 2014 € million | |

|---|---|---|

| Payments for the acquisition of intangible non-current assets | –174 | – |

| Net payments for acquisitions of property, plant and equipment, and investment property (excl. assets subject to operating leases) | –1,433 | –1,144 |

| Changes in the scope of consolidation | –13 | –21 |

| Cash flows from investing activities | –8,253 | –18,526 |

| Proceeds from capital increases | 190 | 384 |

| Proceeds from capital increases by non-controlling interests | – | 144 |

| Dividends paid to shareholders of the Cooperative Financial Network | –567 | –582 |

| Dividends paid to non-controlling interests | –63 | –63 |

| Other payments to non-controlling interests | –248 | – |

| Net change in cash and cash equivalents from other financing activities (including subordinated capital) | 840 | –2,738 |

| Cash flows from financing activities | 152 | –2,855 |

| Cash and cash equivalents as at January 1 | 15,656 | 15,980 |

| Cash flows from operating activities | 12,981 | 21,057 |

| Cash flows from investing activities | –8,253 | –18,526 |

| Cash flows from financing activities | 152 | –2,855 |

| Cash and cash equivalents as at December 31 | 20,536 | 15,656 |

Cash flows from operating activities comprise cash flows mainly arising in connection with the revenue-generating activities of the Cooperative Financial Network or other activities that cannot be classified as investing or financing activities. Cash flows related to the acquisition and sale of non-current assets are allocated to investing activities. Cash flows from financing activities include cash flows arising from transactions with equity owners and from other borrowings to finance business activities.

Notes to the consolidated financial statements

A Significant financial reporting principles

Basis of preparation of the consolidated financial statements

The consolidated financial statements of the Volksbanken Raiffeisenbanken Cooperative Financial Network prepared by the Federal Association of German Cooperative Banks (BVR) are based on the regulations applicable to publicly traded companies. The BVR is under no legal obligation to prepare such consolidated financial statements. The cooperative shares and share capital of the local cooperative banks are held by their members. The local cooperative banks own the share capital of the central institutions either directly or through intermediate holding companies. The Cooperative Financial Network does not qualify as a corporate group as defined by the International Financial Reporting Standards (IFRS), the German Commercial Code (HGB) or the German Stock Corporation Act (AktG).

These consolidated financial statements have been prepared solely for informational purposes and to present the business development and performance of the Cooperative Financial Network, which is treated as a single economic entity in terms of its risks and strategies. These consolidated financial statements are not a substitute for analysis of the consolidated entities' financial statements.

The accounting policies applied in these consolidated financial statements are generally based on the International Financial Reporting Standards.

The underlying data presented in these consolidated financial statements is provided by the separate and consolidated financial statements of the entities in the Cooperative Financial Network and also includes data from supplementary surveys of the local cooperative banks. The consolidated financial statements of DZ BANK and of WGZ BANK included in these consolidated financial statements have been prepared on the basis of IFRS as adopted by the European Union.

As part of the preparation of these consolidated financial statements, the financial statements of the local cooperative banks, of the BVR protection scheme (BVR-SE) and of BVR Institutssicherung GmbH (BVR-ISG), all of which are included and have been prepared in accordance with the German Commercial Code, have been brought into line with IFRSs. Thus, using a simplified approach, assets, liabilities, equity, income and expenses are reconciled to the carrying amounts that would have resulted from consistent application of IFRS.

As in the previous years, certain assumptions and simplifications have been used to prepare these consolidated financial statements. These assumptions and simplifications have been made using tried-andtested methods and have been properly verified. These assumptions and simplifications have been used to eliminate intra-network balances, transactions, income and expenses in a way that reflects the unique structure of the Cooperative Financial Network.

The financial year corresponds to the calendar year. In the interest of clarity, some items on the face of the balance sheet and the income statement have been aggregated and are explained by additional disclosures. Unless stated otherwise, all amounts are shown in millions of euros (€ million). All figures are rounded to the nearest whole number. This may result in very small discrepancies in the calculation of totals and percentages in these consolidated financial statements.

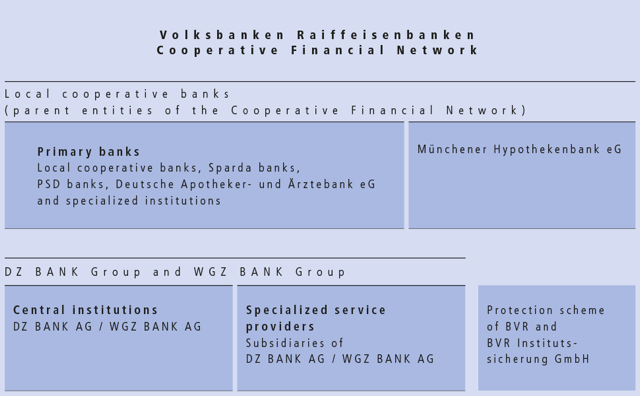

Scope of consolidation

The consolidated entities included in these consolidated financial statements are 1,018 primary banks (2014: 1,036), the DZ BANK Group, the WGZ BANK Group, Münchener Hypothekenbank eG (MHB), the BVR protection scheme, and BVR Institutssicherung GmbH included for the first time in the financial year under review. The consolidated primary banks include Deutsche Apotheker- und Ärztebank eG, the Sparda banks, the PSD banks, and specialized institutions such as BAG Bankaktiengesellschaft.

The primary banks and MHB are the legally independent, horizontally structured parent entities of the Cooperative Financial Network, whereas the other corporate groups and entities are consolidated

as subsidiaries. The two cooperative central institutions and a total of 570 subsidiaries (2014: 622) have been consolidated in the DZ BANK Group and WGZ BANK Group.

The consolidated financial statements include 24 joint ventures between a consolidated entity and at least one other non-network entity (2014: 23) and 31 associates (2014: 25) over which a consolidated entity has significant influence, that are accounted for using the equity method.

Procedures of consolidation

Similar to IFRS 3 in conjunction with IFRS 10, business combinations are accounted for using the purchase method by offsetting the acquisition cost of a subsidiary against the share of the equity that is at tributable to the parent entities and remeasured at fair value on the relevant date when control is acquired. This eliminates the multiple gearing of eligible own funds and any inappropriate creation of own funds for regulatory purposes between the consolidated entities listed above. Any positive difference is recognized as goodwill under other assets and is subject to an annual impairment test. Any negative goodwill is recognized immediately in profit or loss. Any share of subsidiaries' net assets not attributable to the parent entities is reported as non-controlling interests within equity.

Interests in joint ventures and investments in associates are accounted for using the equity method and reported under investments.

The consolidated subsidiaries have generally prepared their financial statements on the basis of the financial year ended December 31, 2015. There is one subsidiary (2014: 1) included in the consolidated financial statements with a different reporting date for its annual financial statements. With 25 exceptions (2014: 20), the separate financial statements of the entities accounted for using the equity method are prepared using the same balance sheet date as that of the consolidated financial statements.

Assets and liabilities as well as income and expenses arising within the Cooperative Financial Network are offset against each other on the basis of certain assumptions and simplifications. Gains and losses arising from transactions between entities within the Cooperative Financial Network are eliminated.

Financial instruments

Financial instruments within the scope of IAS 39 are designated upon initial recognition to the categories defined in IAS 39 on the basis of their characteristics and intended use. IAS 39 defines the following categories:

Financial instruments at fair value through profit or loss

Financial instruments in this category are recognized at fair value through profit or loss. This category is broken down into the following subcategories:

Financial instruments held for trading

The “financial instruments held for trading” subcategory covers financial assets and financial liabilities that are acquired or incurred for the purpose of selling or repurchasing them in the near term, that are part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking, or that are derivatives, except for derivatives that are designated as effective hedging instruments.

Contingent consideration in a business combination

This subcategory includes contingent considerations classified by the acquirer in a business combination as financial assets or financial liabilities.

Financial instruments designated as at fair value through profit or loss; fair value option

Financial assets and financial liabilities may be designated to the “financial instruments designated as at fair value through profit or loss” subcategory by exercising the fair value option, provided that the application of this option eliminates or significantly reduces a measurement or recognition inconsistency (accounting mismatch), the financial assets and liabilities are managed as a portfolio on a fair value basis or they include one or more embedded derivatives required to be separated from the host contract.

Held-to-maturity investments

The “held-to-maturity investments” category consists of non-derivative financial assets with fixed or determinable payments and fixed maturity that an entity has the positive intention and ability to hold to maturity. These investments are measured at amortized cost.

Loans and receivables

The “loans and receivables” category comprises non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables are measured at amortized cost.

Available-for-sale financial assets

“Available-for-sale financial assets” are financial assets that cannot be classified in any other category. In principle, they are measured at fair value. Any changes in fair value occurring between 2 reporting dates are recognized in other comprehensive income. The fair value changes are reported in equity under the “revaluation reserve.” If financial assets included in this category are sold, gains and losses recognized in the revaluation reserve are reclassified to the income statement.

Financial liabilities measured at amortized cost

This category mainly includes all financial liabilities within the scope of IAS 39 that are not held for trading or classified as liabilities measured at fair value through profit or loss.

Other financial instruments

Other financial instruments comprise, for example, insurance-related financial assets and financial liabilities, receivables and liabilities arising from finance leases, or liabilities from financial guarantee contracts.

Recognition and measurement of insurance-related financial assets and financial liabilities as well as receivables and liabilities from finance leases are described in this chapter under the section entitled Insurance business or Leases, respectively.

Liabilities from financial guarantee contracts, that are measured in accordance with IAS 39, have to be recognized by the guarantor at fair value at the time the commitment is made. The fair value normally corresponds to the present value of the consideration received for the assumption of the guarantee. In the context of subsequent measurement, the obligation is to be measured at the higher of a provision recorded in accordance with IAS 37 and the original amount less any amortization recognized subsequently.

Cash and cash equivalents

This item comprises the cash and cash equivalents held by the Cooperative Financial Network. These include cash on hand, balances with central banks and other government institutions as well as public-sector debt instruments and bills of exchange eligible for refinancing by central banks.

Cash on hand comprises euros and other currencies measured at face value or translated at the buying rate. Balances with central banks and other government institutions as well as public-sector debt instruments and bills of exchange eligible for refinancing by central banks are measured at amortized cost.

Loans and advances to banks and customers

All receivables attributable to registered debtors and not classified as “financial assets held for trading” are recognized as loans and advances to banks and customers. In addition to fixed-term receivables and receivables payable on demand in connection with lending, lease, and money market business, loans and advances to banks and customers include promissory notes and registered bonds.

Generally, loans and advances to banks and customers are measured at amortized cost. In fair value hedges, the carrying amounts of hedged receivables are adjusted by the change in the fair value attributable to the hedged risk. To avoid accounting anomalies, certain loans and advances are designated as at fair value through profit or loss. Receivables under finance leases are measured upon initial recognition in the balance sheet at an amount equal to the net investment in the lease at the inception of the lease. Lease payments are apportioned into payment of interest and repayment of principal. The interest portion based on the internal discount rate of the lease transaction for a constant periodic rate of return is recognized as interest income, whereas the repayment of principal reduces the carrying amount of the receivable.

Interest income on loans and advances to banks and customers is recognized as interest income from lending and money market operations. This also includes gains and losses on the amortization of hedge adjustments to carrying amounts due to fair value hedges. Hedge adjustments are recognized

within other gains and losses on valuation of financial instruments under gains and losses arising on hedging transactions. Gains and losses on loans and advances designated as at fair value through profit or loss are also recognized in other gains and losses on valuation of financial instruments.

Allowances for losses on loans and advances

Financial assets not measured at fair value through profit or loss have to be reviewed at each reporting date to determine whether there is objective evidence of impairment. If such objective evidence is available, specific allowances in the amount of the determined impairment loss requirement are recognized for financial assets. Financial assets with similar features for which impairment losses are not recognized on an individual basis are grouped into portfolios and assessed collectively for possible impairment. Impairment losses are calculated on the basis of historical default rates for comparable portfolios. If any impairment is identified, a portfolio loan loss allowance is recognized.

The allowance for losses on loans and advances to banks and to customers is reported as a separate line item on the assets side of the balance sheet. Additions to and reversals of allowances for losses on loans and advances to banks and to customers are recognized in the income statement under allowances for losses on loans and advances.

The recognition of allowances for losses on loans and advances in the Cooperative Financial Network also includes changes in the provisions for loan commitments, other provisions for loans and advances, and liabilities from financial guarantee contracts. Additions to and reversals of these items are also recognized in the income statement under allowance for losses on loans and advances.

Derivatives used for hedging (positive and negative fair values)

Derivatives used for hedging (positive and negative market values) include the carrying amounts of derivative financial instruments designated as hedging instruments in an effective and documented hedging relationship within the meaning of IAS 39.

The derivative financial instruments are measured at fair value. Changes in the fair value of hedging instruments used to hedge the fair value of hedged items are recognized in the income statement. If the hedging instruments are intended as a cash flow hedge or a hedge of a net investment in a foreign operation, changes in fair value attributable to the effective portion of the hedge are recognized as other comprehensive income.

Financial assets and financial liabilities held for trading

Financial assets and financial liabilities held for trading include derivatives with positive and negative fair values that were entered into for trading purposes or that do not meet the requirements for an accounting treatment as hedging instruments.

Financial assets held for trading also include securities and loans and advances which are held for trading purposes as well as items related to commodities transactions. The loans and advances include promissory notes, registered bonds and money market receivables.

Apart from derivative financial instruments with negative fair values, financial liabilities held for trading include delivery commitments arising from the short-selling of securities, bonds issued and other debt certificates entered into for trading purposes, liabilities and obligations from commodities transactions. Bonds issued and other debt certificates include share- and index-linked certificates as well as commercial papers. Liabilities result primarily from money market transactions.

Financial assets and financial liabilities held for trading are recognized at fair value through profit or loss. Generally, gains and losses on financial instruments reported as financial assets or financial liabilities held for trading are recognized as gains and losses on trading activities.

Gains and losses on the valuation of derivative financial instruments entered into for hedging purposes, but that do not meet the requirements for classification as a hedging instrument, are recognized under other gains and losses on valuation of financial instruments as gains and losses on derivatives held for purposes other than trading. If, to avoid accounting

mismatches, hedged items are classified as financial instruments designated as at fair value through profit or loss’, the valuation gains and losses on the related derivatives concluded for economic hedging purposes are recognized under gains and losses on financial instruments designated as at fair value through profit or loss.

Investments

Investments include securities, shareholdings in subsidiaries and equity investments. Securities comprise bearer bonds and other fixed-income securities as well as shares and other non-fixed-income securities. Investments also include shares in unconsolidated subsidiaries. Equity investments consist of other shareholdings in companies in bearer or registered form where no significant influence exists, as well as interests in joint ventures and associates.

Generally, investments are initially recognized at fair value. Shares, investments in subsidiaries, joint ventures and associates, and other shareholdings for which a fair value cannot be reliably determined or which are accounted for using the equity method are initially recognized at cost.

Property, plant and equipment, and investment property

Property, plant and equipment, and investment property comprise land and buildings, office furniture and equipment, and other fixed assets with an estimated useful life of more than one reporting period used by the Cooperative Financial Network. This item also includes assets subject to operating leases. Investment property is real estate held for the purposes of generating rental income or capital appreciation.

Property, plant and equipment, and investment property is measured at cost less cumulative depreciation and impairment losses in subsequent reporting periods.

Depreciation and impairment losses on property, plant and equipment, and investment property are recognized as administrative expenses. Reversals of impairment losses are reported under other net operating expense/income.

Income tax assets and liabilities

Current and deferred tax assets are shown under the income tax assets balance sheet item; current and deferred tax liabilities are reported under the balance sheet item Income tax liabilities. Current income tax assets and liabilities are recognized in the amount of any expected refund or future payment.

Deferred tax assets and liabilities are recognized for temporary differences between the carrying amounts recognized in the consolidated financial statements and those of assets and liabilities recognized in the financial statements for tax purposes. Deferred tax assets are also recognized in respect of as yet unused tax loss carryforwards, provided that utilization of these loss carryforwards is sufficiently probable. Deferred tax assets are measured using the national and company-specific tax rates expected to apply at the time of realization.

Deferred tax assets and liabilities are not discounted. Where temporary differences arise in relation to items recognized in other comprehensive income, the resulting deferred tax assets and liabilities are also recognized in other comprehensive income. Current and deferred tax income and expense to be recognized through profit or loss is reported under income taxes in the income statement.

Other assets

Other assets include a number of items, including intangible assets. Intangible assets are recognized at cost. In the subsequent measurement of software, acquired customer relationships, and other intangible assets with a finite useful life, carrying amounts are reduced by cumulative amortization and cumulative impairment losses. Goodwill and other intangible assets with an indefinite useful life are not amortized, but are subject to an impairment test at least once during the financial year.

Deposits from banks and customers

All liabilities attributable to registered creditors and not classified as “financial liabilities held for trading” are recognized as deposits from banks and customers. In addition to fixed-maturity liabilities and liabilities repayable on demand arising from the deposit, home savings and money market businesses,

these liabilities include, above all, registered bonds and promissory notes issued.

Deposits from banks and customers are measured at amortized cost. Where deposits from banks and amounts owed to other depositors are designated as a hedged item in an effective fair value hedge, the carrying amount is adjusted for any change in the fair value attributable to the hedged risk. To avoid accounting mismatches, certain liabilities are designated as at fair value through profit or loss.

Interest expense on deposits from banks and customers are recognized separately under net interest income. Interest expense also includes gains and losses on early repayment and on the amortization of hedge adjustments to carrying amounts due to fair value hedges. Hedge adjustments to the carrying amount due to fair value hedges are reported within other gains and losses on valuation of financial instruments under gains and losses arising on hedging transactions. Gains and losses on liabilities designated as at fair value through profit or loss are also recognized in other gains and losses on valuation of financial instruments.

Debt certificates issued including bonds

Debt certificates including bonds cover issued Pfandbriefe, other bonds and other debt certificates evidenced by paper for which transferable bearer certificates have been issued.

Debt certificates and gains and losses on these certificates are measured and recognized in the same way as deposits from banks and customers.

Provisions

Provisions are recognized for defined benefit obligations, within the context of the lending and home savings businesses, as well as for other uncertain liabilities to third parties.

Actuarial reports are used to calculate the carrying amounts of defined benefit obligations. These include assumptions about long-term salary and pension trends and average life expectancy. Assumptions about salary and pension trends are based on past trends and take account of expectations about future labor market trends. Recognized biometric tables (mortality tables published by Professor

Dr. Klaus Heubeck) are used to estimate average life expectancy. The discount rate used to discount future payment obligations is an appropriate market interest rate as at the reporting date for high-quality fixed-income corporate bonds with a maturity equivalent to that of the defined benefit obligations. Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions regarding defined benefit obligations as well as gains and losses on remeasurements of plan assets are recognized as other comprehensive income in the financial year in which they occur.

Other provisions are measured based on the best estimate of the present value of their anticipated utilization, taking into account risks and uncertainties associated with the issues concerned as well as future events. The outflows of funds actually materializing in future may differ from the estimated utilization of provisions. Provisions for loans and advances factor in the usual sector-specific level of uncertainty about amounts and maturity dates.

Provisions relating to building society operations are recognized to cover the payment of any bonuses that may have been agreed in the terms and conditions of home savings contracts. These bonuses may take the form of a reimbursement of some of the sales charges or interest bonuses on deposits. The bonuses constitute independent payment obligations and must be measured and recognized in accordance with IAS 37. In order to measure these obligations, building society simulations (collective simulations) are used to forecast building society customers’ future behavior. Uncertainty in connection with the measurement of these provisions is linked to assumptions to be made about future customer behavior, which take account of various scenarios and measures. Material inputs for the collective simulations are the rate of mortgage loans not drawn down and the pattern of customer cancellations.

Provisions are recognized for risks arising from ongoing legal disputes and cover the possible resulting losses. Such provisions are recognized when it is more likely than not that a legal dispute will result in a payment obligation for an entity in the BVR. Any concentration risk owing to similarities between individual cases is taken into consideration.

Subordinated capital

Subordinated capital comprises all debt instruments in bearer or registered form that, in the event of insolvency or liquidation, are repaid only after settlement of all unsubordinated liabilities but before distribution to shareholders of any proceeds from the insolvency or liquidation.

Subordinated capital comprises subordinated liabilities and profit-sharing rights as well as regulatory core capital not included in equity, which is recognized as hybrid capital. The share capital repayable on demand comprises non-controlling interests in partnerships controlled by companies in the Cooperative Financial Network. These non-controlling interests must be classified as subordinated.

Subordinated capital and gains and losses on these certificates are measured and recognized in the same way as deposits from banks and customers.

Equity

Equity represents the residual value of the Cooperative Financial Network's assets minus its liabilities. Cooperative shares of the independent local cooperative banks and capital of silent partners are treated as economic equity in the consolidated financial statements and are recognized as equity. Equity thus comprises subscribed capital – consisting of cooperative shares or share capital and capital of silent partners – plus capital reserves of the local cooperative banks. It also includes equity earned by the Cooperative Financial Network, the reserve resulting from the fair value measurement of available-for-sale financial assets (revaluation reserve), the cash flow hedge reserve, the currency translation reserve, and the non-controlling interests in the equity of consolidated subsidiaries.

Trust activities

Trust activities are defined as business transacted on one's own behalf for a third-party account. Assets and liabilities held as part of trust activities do not satisfy the criteria for recognition on the balance sheet.

Income and expenses arising from trust activities are recognized as fee and commission income or as fee and commission expenses. Income and expenses resulting from the passing-through and administration of trust loans are netted and are included in the fee and commission income earned from lending and trust activities.

Insurance business

Insurance business in the Cooperative Financial Network is generally reported under specific insurance items on the face of the income statement and balance sheet.

Financial assets and financial liabilities

Financial assets and financial liabilities held or entered into in connection with insurance operations are generally accounted for and measured in accordance with IAS 39. They are reported in the investments held by insurance companies, or in the other assets and other liabilities of insurance companies. Impairment losses on financial assets recognized under the investments and the other assets of insurance companies are directly deducted from the assets' carrying amounts.

In addition to financial instruments within the scope of IAS 39, certain financial assets and financial liabilities are held as part of the insurance business and, as required by IFRS 4.25(c), are recognized and measured in accordance with the provisions of the HGB and other German accounting standards applicable to insurance companies. These financial assets and financial liabilities include deposits with ceding insurers, deposits received from reinsurers, receivables and payables arising out of direct insurance operations, and assets related to unit-linked contracts.

Insurance liabilities

Insurance companies are permitted to continue applying existing accounting policies to certain insurance-specific items during a transition period. Insurance liabilities are therefore recognized and measured in accordance with the provisions of the HGB and other German accounting standards applicable to insurance companies. Insurance liabilities are shown before the deduction of the share of reinsurers, which is reported as an asset.

Leases

A lease is classified as a finance lease if substantially all the risks and rewards incidental to the ownership of an asset are transferred from the lessor to the lessee. If a lease is classified as a finance lease, a receivable due from the lessee must be recognized. The receivable is measured at an amount equal to the net investment in the lease at the inception of the lease. Lease payments are apportioned into payment of interest and repayment of principal. Revenue is recognized as interest income on an accrual basis.

B Selected disclosures of interests in other entities

Investments in subsidiaries

Share in the business operations of the Cooperative Financial Network attributable to non-controlling interests

DZ BANK AG Deutsche Zentral-Genossenschaftsbank (DZ BANK) and Westdeutsche Genossenschafts-Zentralbank AG (WGZ BANK) are included in the consolidated financial statements together with their respective subsidiaries as a subgroup. In this context, DZ BANK and WGZ BANK are focused on their clients and owners, the local cooperative banks, as central bank, commercial bank and holding company. The objective of this focus is to sustainably expand the position of the Cooperative Financial Network as one of the leading universal financial service groups.

The shares of DZ BANK, with its headquarters in Frankfurt/Main, Germany, are held by the primary banks and by MHB, with ownership interests amounting to 86.2 percent (2014: 85.4 percent). Another 6.7 percent (2014: 6.7 percent) of the shares are held by WGZ BANK. The remaining shares of 7.1 percent (2014: 7.9 percent) are attributable to shareholders that are not part of the Cooperative Financial Network. The pro-rata share in net profit attributable to non-controlling interests amounts to €191 million (2014: €241 million). The carrying amount of non-controlling interests amounts to €2,836 million (2014: €3,279 million). In the financial year under review, the dividend payment made to non-controlling interests amounts to €62 million (2014: €62 million).

The shares of WGZ BANK, with its headquarters in Düsseldorf, Germany, are held by the primary banks with ownership interests amounting to 98.1 percent (2014: 98.1 percent). The remaining shares of 1.9 percent (2014: 1.9 percent) are attributable to shareholders that are not part of the Cooperative Financial Network. The pro-rata share in net profit attributable to non-controlling interests amounts to €15 million (2014: €11 million). The carrying amount of non-controlling interests amounts to €83 million (2014: €69 million). In the financial year under review, the dividend payment made to non-controlling interests amounts to €1 million, unchanged from the prior year.

Nature and extent of significant restrictions

National regulatory requirements, contractual provisions, and provisions of company law restrict the ability of the DZ BANK Group companies included in the consolidated financial statements to transfer assets within the group. Prior-year amounts were adjusted as a result of the reassessment of the nature and extent of significant restrictions. Where restrictions can be specifically assigned to individual line items on the balance sheet, the carrying amounts of the assets subject to restrictions on the balance sheet date are shown in the following table:

| Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) | |

|---|---|---|---|

| Assets | 74,732 | 70,721 | 5.7 |

| Loans and advances to customers | 4,174 | 4,944 | –15.6 |

| Investments held by insurance companies | 70,552 | 65,770 | 7.3 |

| Other assets | 6 | 7 | –14.3 |

| Liabilities | 119,148 | 112,392 | 6.0 |

| Deposits from banks | 1,690 | 1,583 | 6.8 |

| Deposits from customers | 50,926 | 48,343 | 5.3 |

| Provisions | 653 | 580 | 12.6 |

| Insurance liabilities | 65,879 | 61,886 | 6.5 |

Nature of the risks associated with interests in consolidated structured entities

Risks arising from interests in consolidated structured entities largely result from loans to fully consolidated funds within the DZ BANK Group, some of which are extended in the form of junior loans.

Interests in joint arrangements and investments in associates

Nature, extent and financial effects of interests in joint arrangements

The carrying amount of individually immaterial joint ventures accounted for using the equity method totaled €564 million as at the balance sheet date (2014: €615 million).

Aggregated financial information for joint ventures accounted for using the equity method that individually are not material:

| 2015 € million | 2014 € million | Change (percent) | |

|---|---|---|---|

| Share of profit from continuing operations | 110 | 95 | 15.8 |

| Share of other comprehensive income/loss | 24 | 56 | –57.1 |

| Pro-rata share of total comprehensive income/loss | 134 | 151 | –11.3 |

Nature, extent and financial effects of interests in associates

The carrying amount of individually immaterial associates accounted for using the equity method totaled €410 million as at the balance sheet date (2014: €369 million).

Aggregated financial information for associates accounted for using the equity method that individually are not material:

| 2015 € million | 2014 € million | Change (percent) | |

|---|---|---|---|

| Share of profit from continuing operations | 17 | 21 | –19.0 |

| Share of profit from discontinued operations | 1 | 1 | – |

| Share of other comprehensive income/loss | 22 | –6 | >100.0 |

| Pro-rata share of total comprehensive income/loss | 40 | 16 | >100.0 |

Interests in unconsolidated structured entities

Structured entities are entities that have been designed so that voting rights or similar rights are not the dominant factor in deciding who controls the entity. The Cooperative Financial Network mainly distinguishes between the following types of interests in unconsolidated structured entities, based on their design and the related risks; these entities largely concern companies of the DZ BANK Group: – Interests in investment funds issued by the Cooperative Financial Network, – Interests in investment funds not issued by the Cooperative Financial Network, – Interests in securitization vehicles, – Interests in asset-leasing vehicles

Interests in investment funds issued by the Cooperative Financial Network

The interests in the investment funds issued by the Cooperative Financial Network largely comprise investment funds issued by entities in the Union Investment Group in accordance with the contractual form model without voting rights and, to a lesser extent, those that are structured as a company with a separate legal personality. Furthermore, the DVB Bank Group makes subordinated loans available to fully consolidated funds for the purpose of transport finance. In turn, these funds make subordinated loans or direct equity investments available to unconsolidated entities.

The maximum exposure of the investment funds issued and managed by the DZ BANK Group is determined as a gross value, excluding deduction of available collateral, and amounts to €10,331 million as at the reporting date (2014: €11,509 million). These investment fund assets resulted in losses of €15 million (2014: losses of €5 million) as well as income of €1,636 million (2014: €1,445 million).

Interests in investment funds not issued by the Cooperative Financial Network

The interests in the investment funds not issued by the Cooperative Financial Network above all comprise investment funds managed by entities in the Union Investment Group within the scope of their own decision-making powers that have been issued by entities outside the Cooperative Financial Network and parts of such investment funds.

Their total volume amounted to €27,269 million (2014: €24,289 mil -lion). The DZ BANK Group also extends loans to investment funds in order to generate interest income. In addition, there are investment funds issued by entities outside the Cooperative Financial Network in connection with unit-linked life insurance of the R+V Group (R+V) amounting to €7,351 million (2014: €2,088 million) that, however, do not result in a maximum exposure.

The maximum exposure arising from the investment funds not issued by the DZ BANK Group is determined as a gross value, excluding deduction of available collateral, and amounts to €2,095 million as at the reporting date (2014: €1,816 million). Income generated from these investment fund assets in the financial year 2015 amounted to €108 million (2014: €108 million).

Interests in securitization vehicles

The interests in securitization vehicles are interests in vehicles where the DZ BANK Group’s involvement goes beyond that of an investor.

The material interests in securitization vehicles comprise the two multi-seller ABCP programs: CORAL and AUTOBAHN. DZ BANK acts as sponsor and program agent for both programs. It is also the program administrator for AUTOBAHN.

The maximum exposure of the interests in securitization vehicles in the DZ BANK Group is determined as a gross value, excluding deduction of available collateral, and amounts to €3,459 million as at the reporting date (2014: €3,283 million). Income generated from these interests in the financial year 2015 amounted to €84 million (2014: €85 million).

Interests in asset-leasing vehicles

The interests in asset-leasing vehicles comprise shares in limited partnerships and voting rights, other than the shares in limited partnerships, in partnerships established by VR LEASING for the purpose of real estate leasing (asset-leasing vehicles), in which the asset, and the funding occasionally provided by the DZ BANK Group, are placed.

The actual maximum exposure of the interests in asset-leasing vehicles in the DZ BANK Group is determined as a gross value, excluding deduction of available collateral, and amounts to €1 million as at the reporting date. Interest income and current income and expense generated from these interests in the financial year 2015 amounted to €5 million (2014: €3 million).

C Income statement disclosures

| 1. Information on operating segments Financial year 2015 (€ million) | Bank | Retail | Real Estate Finance | Insurance | Other/Consolidation | Total |

|---|---|---|---|---|---|---|

| Net interest income | 2,017 | 17,260 | 1,593 | – | –849 | 20,021 |

| Allowances for losses on loans and advances | –94 | –7 | 27 | – | – | –74 |

| Net fee and commission income | 586 | 5,911 | –193 | – | –506 | 5,798 |

| Gains and losses on trading activities | 458 | 189 | –19 | – | –21 | 607 |

| Gains and losses on investments | 110 | –611 | –53 | – | –7 | –561 |

| Other gains and losses on valuation of financial instruments | 7 | –6 | 364 | – | –2 | 363 |

| Premiums earned | – | – | – | 14,418 | – | 14,418 |

| Gains and losses on investments held by insurance companies and other insurance company gains and losses | – | – | – | 3,132 | –119 | 3,013 |

| Insurance benefit payments | – | – | – | –14,664 | – | –14,664 |

| Insurance business operating expenses | – | – | – | –2,287 | 513 | –1,774 |

| Administrative expenses | –1,830 | –15,119 | –700 | – | 415 | –17,234 |

| Other net operating expense/income | –98 | –68 | 31 | 26 | –17 | –126 |

| Profit/loss before taxes | 1,156 | 7,549 | 1,050 | 625 | –593 | 9,787 |

| Cost/income ratio (percent) | 59.4 | 66.7 | 40.6 | – | – | 63.6 |

| Financial year 2014 € million | Bank | Retail | Real Estate Finance | Insurance | Other/Consolidation | Total |

|---|---|---|---|---|---|---|

| Net interest income | 1,917 | 17,277 | 1,552 | – | –699 | 20,047 |

| Allowances for losses on loans and advances | –147 | –174 | 9 | – | 13 | –299 |

| Net fee and commission income | 576 | 5,542 | –146 | – | –505 | 5,467 |

| Gains and losses on trading activities | 570 | 210 | –18 | – | –10 | 752 |

| Gains and losses on investments | 61 | 54 | 8 | – | 25 | 148 |

| Other gains and losses on valuation of financial instruments | –39 | 12 | 454 | – | 8 | 435 |

| Premiums earned | – | – | – | 13,927 | – | 13,927 |

| Gains and losses on investments held by insurance companies and other insurance company gains and losses | – | – | – | 4,481 | –93 | 4,388 |

| Insurance benefit payments | – | – | – | –15,264 | – | –15,264 |

| Insurance business operating expenses | – | – | – | –2,284 | 514 | –1,770 |

| Administrative expenses | –1,675 | –14,880 | –735 | – | 395 | –16,895 |

| Other net operating expense/income | –167 | –196 | 57 | –4 | 29 | –281 |

| Profit/loss before taxes | 1,096 | 7,845 | 1,181 | 856 | –323 | 10,655 |

| Cost/income ratio (percent) | 57.4 | 65.0 | 38.5 | – | – | 60.7 |

Definition of operating segments

The Volksbanken Raiffeisenbanken Cooperative Financial Network is founded on the underlying principle of decentralization. It is based on the local primary banks, whose business activities are supported by the two central institutions – DZ BANK and WGZ BANK – and by specialized service providers within the cooperative sector. These specialized service providers are integrated into the central institutions. The main benefit derived by the primary banks from their collaboration with these specialized services providers and the central institutions is that they can offer a full range of financial products and services.

The Bank operating segment combines the activities of the Cooperative Financial Network in the corporate customers, institutional customers and capital markets businesses. The operating segment focuses on corporate customers. It essentially comprises DZ BANK, WGZ BANK, the VR LEASING Group, the DVB Bank Group, DZ BANK Ireland plc, and WGZ BANK Ireland plc.

The Retail operating segment covers private banking and activities relating to asset management. The segment focuses on retail clients. It mainly includes primary banks as well as the DZ PRIVATBANK, TeamBank AG Nürnberg (TeamBank) and Union Investment Group.

The Real Estate Finance operating segment encompasses the home savings and loan operations, mortgage banking, and real estate business. The entities allocated to this operating segment include Bausparkasse Schwäbisch Hall Group (BSH), Deutsche Genossenschafts-Hypothekenbank AG, WL BANK AG Westfälische Landschaft Bodenkreditbank, and MHB.

Insurance operations are reported under the Insurance operating segment. This operating segment consists solely of R+V.

Other/Consolidation contains the BVR protection scheme (BVR-SE) as well as BVR Institutssicherung GmbH (BVR-ISG), whose task is to avert impending or existing financial difficulties faced by member institutions by taking preventive action or implementing restructuring measures. This operating segment also includes intersegment consolidation items.

Presentation of the disclosures on operating segments

The information on operating segments presents the interest income generated by the operating segments and the associated interest expenses on a netted basis as net interest income.

Intersegment consolidation

The adjustments to the figure for net interest income resulted largely from the consolidation of dividends paid within the Cooperative Financial Network.

The figure under Other/Consolidation for net fee and commission income relates specifically to the fee and commission business transacted between the primary banks, TeamBank, BSH, and R+V.

The figure under Other/Consolidation for administrative expenses includes the contributions paid to BVR-SE and BVR-ISG by member institutions of the Cooperative Financial Network.

The remaining adjustments are largely attributable to the consolidation of income and expenses.

| 2. Net interest income | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Interest income and current income and expense | 28,792 | 30,657 | –6.1 |

| Interest income from | 27,396 | 29,307 | –6.5 |

| Lending and money market business | 24,307 | 25,709 | –5.5 |

| of which building society operations | 1,031 | 1,008 | 2.3 |

| Finance leases | 184 | 232 | –20.7 |

| Fixed-income securities | 3,646 | 4,121 | –11.5 |

| Other assets | –538 | –523 | 2.9 |

| Financial assets with a negative effective interest rate | –19 | – | – |

| Current income from | 1,267 | 1,224 | 3.5 |

| Shares and other variable-yield securities | 1,023 | 1,144 | –10.6 |

| Investments in subsidiaries and equity investments | 264 | 89 | >100.0 |

| Operating leases | –20 | –9 | >100.0 |

| Income/loss from using the equity method for | 48 | 46 | 4.3 |

| Investment in joint ventures | 41 | 36 | 13.9 |

| Investments in associates | 7 | 10 | –30.0 |

| Income from profit-pooling, profit-transfer and partial profit-transfer agreements | 81 | 80 | 1.3 |

| Interest expense | –8,771 | –10,610 | –17.3 |

| Interest expense on | –8,506 | –9,964 | –14.6 |

| Deposits from banks and customers | –6,424 | –7,882 | –18.5 |

| of which: building society operations | –820 | –773 | 6.1 |

| Debt certificates including bonds | –1,887 | –1,825 | 3.4 |

| Subordinated capital | –241 | –297 | –18.9 |

| Other liabilities | 19 | 40 | –52.5 |

| Financial liabilities with a positive effective interest rate | 27 | – | – |

| Other interest expense | –265 | –646 | –59.0 |

| Total | 20,021 | 20,047 | –0.1 |

The interest income from other assets and the interest expense on other liabilities result from gains and losses on the amortization of fair value changes of the hedged items in portfolio hedges of interest-rate risk. Owing to the current low level of interest rates in the money markets and capital markets, there may be a negative effective interest rate for financial assets and a positive effective interest rate for financial liabilities. In 2014, these effects were shown in net fee and commission income.

| 3. Allowances for losses on loans and advances | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Additions | –2,143 | –2,467 | –13.1 |

| Reversals | 1,906 | 2,092 | –8.9 |

| Directly recognized impairment losses | –167 | –187 | –10.7 |

| Recoveries from loans and advances previously impaired | 318 | 296 | 7.4 |

| Changes in the provisions for loans and advances as well as in the liabilities from financial guarantee contracts | 12 | –27 | >100.0 |

| Impairment losses on loans and advances available for sale | – | –6 | 100.0 |

| Total | –74 | –299 | –75.3 |

| 4. Net fee and commission income | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Fee and commission income | 7,292 | 6,793 | 7.3 |

| Securities business | 3,278 | 2,912 | 12.6 |

| Asset management | 346 | 283 | 22.3 |

| Payments processing including card processing | 2,398 | 2,345 | 2.3 |

| Lending business and trust activities | 262 | 264 | –0.8 |

| Financial guarantee contracts and loan commitments | 181 | 182 | –0.5 |

| Foreign commercial business | 134 | 112 | 19.6 |

| Building society operations | 5 | 29 | –82.8 |

| Other | 688 | 663 | 3.8 |

| Income from negative effective interest rates for financial liabilities | – | 3 | –100.0 |

| Fee and commission expense | –1,494 | –1,326 | 12.7 |

| Securities business | –491 | –423 | 16.1 |

| Asset management | –116 | –89 | 30.3 |

| Payments processing including card processing | –284 | –286 | –0.7 |

| Lending business and trust activities | –165 | –117 | 41.0 |

| Financial guarantee contracts and loan commitments | 51 | –11 | >100.0 |

| International business | –28 | –22 | 27.3 |

| Building society operations | –103 | –129 | –20.2 |

| Other | –358 | –248 | 44.4 |

| Expenses from negative effective interest rates for financial assets | – | –1 | 100.0 |

| Total | 5,798 | 5,467 | 6.1 |

The income from negative effective interest rates for financial liabilities and the expenses from negative effective interest rates for financial assets were presented in net interest income in 2015.

| 5. Gains and losses on trading activities | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Gains and losses on trading in financial instruments | 287 | 637 | –54.9 |

| Gains and losses on trading in foreign exchange, foreign notes and coins, and precious metals | 135 | –74 | >100.0 |

| Gains and losses on commodities trading | 185 | 189 | –2.1 |

| Total | 607 | 752 | –19.3 |

| 6. Gains and losses on investments | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Gains and losses on securities | –636 | 83 | >100.0 |

| Gains and losses on investments in subsidiaries and equity investments | 75 | 65 | 15.4 |

| Total | –561 | 148 | >100.0 |

| 7. Other gains and losses on valuation of financial instruments | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Gains and losses from hedge accounting | 31 | –27 | >100,0 |

| Fair value hedges | 31 | –27 | >100,0 |

| Gains and losses on hedging instruments | 1.895 | –3.776 | >100,0 |

| Gains and losses on hedged items | –1.864 | 3.749 | >100,0 |

| Gains and losses on derivatives held for purposes other than trading | –86 | 2 | >100,0 |

| Gains and losses on financial instruments designated as at fair value through profit or loss | 418 | 460 | –9,1 |

| Total | 363 | 435 | –16,6 |

| 8. Premiums earned | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Net premiums written | 14,442 | 13,957 | 3.5 |

| Gross premiums written | 14,536 | 14,040 | 3.5 |

| Reinsurance premiums ceded | –94 | –83 | 13.3 |

| Change in provision for unearned premiums | –24 | –30 | –20.0 |

| Gross premiums | –26 | –29 | –10.3 |

| Reinsurers' share | 2 | –1 | >100.0 |

| Total | 14,418 | 13,927 | 3.5 |

| 9. Gains and losses on investments held by insurance companies and other insurance company gains and losses | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Interest income and current income | 2,575 | 2,587 | –0.5 |

| Administrative expenses | –115 | –122 | –5.7 |

| Gains and losses on valuation and disposals | 478 | 1,809 | –73.6 |

| Other gains and losses of insurance companies | 75 | 114 | –34.2 |

| Total | 3,013 | 4,388 | –31.3 |

| 10. Insurance benefit payments | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Expenses for claims | –9,850 | –9,487 | 3.8 |

| Gross expenses for claims | –9,890 | –9,524 | 3.8 |

| Reinsurers' share | 40 | 37 | 8.1 |

| Changes in benefit reserve, provisions for premium refunds and in other insurance liabilities | –4,814 | –5,777 | –16.7 |

| Changes in gross liabilities | –4,808 | –5,765 | –16.6 |

| Reinsurers' share | –6 | –12 | –50.0 |

| Total | –14,664 | –15,264 | –3.9 |

Claims rate trend for direct non-life insurance business including claim settlement costs

Gross claims provisions in direct business and payments made against the original provisions:

| € million | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| At the end of the year | 3,856 | 3,634 | 3,901 | 3,345 | 3,341 | 3,324 | 2,953 | 2,704 | 2,672 | 2,509 | 2,396 |

| 1 year later | – | 3,523 | 3,847 | 3,336 | 3,359 | 3,135 | 2,901 | 2,623 | 2,601 | 2,414 | 2,253 |

| 2 years later | – | – | 3,769 | 3,247 | 3,279 | 3,160 | 2,763 | 2,527 | 2,531 | 2,306 | 2,170 |

| 3 years later | – | – | – | 3,220 | 3,254 | 3,139 | 2,756 | 2,533 | 2,472 | 2,268 | 2,127 |

| 4 years later | – | – | – | – | 3,241 | 3,122 | 2,756 | 2,505 | 2,487 | 2,230 | 2,110 |

| 5 years later | – | – | – | – | – | 3,139 | 2,768 | 2,513 | 2,478 | 2,245 | 2,088 |

| 6 years later | – | – | – | – | – | – | 2,710 | 2,469 | 2,434 | 2,214 | 2,085 |

| 7 years later | – | – | – | – | – | – | – | 2,466 | 2,422 | 2,210 | 2,056 |

| 8 years later | – | – | – | – | – | – | – | – | 2,426 | 2,205 | 2,048 |

| 9 years later | – | – | – | – | – | – | – | – | – | 2,207 | 2,042 |

| 10 years later | – | – | – | – | – | – | – | – | – | – | 2,048 |

| Settlements | – | 111 | 132 | 125 | 100 | 185 | 243 | 238 | 246 | 302 | 348 |

The figures for the Condor non-life insurance companies are included from 2009.

Net claims provisions in direct business and payments made against the original provisions:

| € million | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 |

|---|---|---|---|---|---|---|

| At the end of the year | 3,827 | 3,574 | 3,669 | 3,313 | 3,298 | 3,254 |

| 1 year later | – | 3,460 | 3,613 | 3,300 | 3,317 | 3,056 |

| 2 years later | – | – | 3,533 | 3,211 | 3,236 | 3,077 |

| 3 years later | – | – | – | 3,180 | 3,208 | 3,057 |

| 4 years later | – | – | – | – | 3,194 | 2,939 |

| 5 years later | – | – | – | – | – | 3,049 |

| Settlements | – | 114 | 136 | 133 | 104 | 205 |

Claims rate trend for inward reinsurance business

Gross claims provisions in inward reinsurance business and payments made against the original provisions:

| € million | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Gross provisions for claims outstanding | 2,433 | 1,976 | 1,710 | 1,506 | 1,409 | 1,190 | 892 | 712 | 596 | 524 | 504 |

| Cumulative payments for the year concerned and prior years | |||||||||||

| 1 year later | – | 464 | 481 | 385 | 463 | 437 | 282 | 232 | 127 | 138 | 134 |

| 2 years later | – | – | 685 | 630 | 640 | 632 | 399 | 347 | 203 | 175 | 179 |

| 3 years later | – | – | – | 764 | 345 | 739 | 468 | 410 | 250 | 212 | 208 |

| 4 years later | – | – | – | – | 891 | 856 | 516 | 447 | 282 | 240 | 224 |

| 5 years later | – | – | – | – | – | 922 | 588 | 475 | 307 | 252 | 246 |

| 6 years later | – | – | – | – | – | – | 626 | 528 | 324 | 266 | 252 |

| 7 years later | – | – | – | – | – | – | – | 555 | 366 | 283 | 265 |

| 8 years later | – | – | – | – | – | – | – | – | 384 | 307 | 276 |

| 9 years later | – | – | – | – | – | – | – | – | – | 321 | 295 |

| 10 years later | – | – | – | – | – | – | – | – | – | – | 305 |

| Gross provisions for claims outstanding and payments made against the original provision | |||||||||||

| At the end of the year | 2,433 | 1,976 | 1,710 | 1,506 | 1,409 | 1,190 | 892 | 712 | 596 | 524 | 504 |

| 1 year later | – | 2,157 | 1,840 | 1,593 | 1,536 | 1,401 | 1,026 | 779 | 583 | 541 | 497 |

| 2 years later | – | – | 1,859 | 1,569 | 1,472 | 1,343 | 872 | 765 | 529 | 480 | 461 |

| 3 years later | – | – | – | 1,628 | 1,014 | 1,338 | 826 | 696 | 518 | 432 | 420 |

| 4 years later | – | – | – | – | 1,528 | 1,360 | 837 | 680 | 479 | 423 | 382 |

| 5 years later | – | – | – | – | – | 1,396 | 858 | 691 | 470 | 396 | 381 |

| 6 years later | – | – | – | – | – | – | 870 | 709 | 480 | 391 | 362 |

| 7 years later | – | – | – | – | – | – | – | 719 | 498 | 399 | 360 |

| 8 years later | – | – | – | – | – | – | – | – | 504 | 403 | 367 |

| 9 years later | – | – | – | – | – | – | – | – | – | 407 | 368 |

| 10 years later | – | – | – | – | – | – | – | – | – | – | 372 |

| Settlements | – | –181 | –149 | –122 | –119 | –206 | 22 | –7 | 92 | 117 | 132 |

The figures for the Condor non-life insurance companies are included from 2009.

Net claims provisions in inward reinsurance business and payments made against the original provisions:

| € million | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 |

|---|---|---|---|---|---|---|

| Net provisions for claims outstanding | 2,428 | 1,970 | 1,695 | 1,491 | 1,389 | 1,164 |

| Cumulative payments for the year concerned and prior years | ||||||

| 1 year later | – | 464 | 473 | 383 | 461 | 432 |

| 2 years later | – | – | 677 | 620 | 636 | 625 |

| 3 years later | – | – | – | 754 | 333 | 729 |

| 4 years later | – | – | – | – | 878 | 839 |

| 5 years later | – | – | – | – | – | 904 |

| Net provisions for claims outstanding and payments made against the original provision | ||||||

| At the end of the year | 2,428 | 1,970 | 1,695 | 1,491 | 1,389 | 1,164 |

| 1 year later | – | 2,152 | 1,827 | 1,576 | 1,519 | 1,377 |

| 2 years later | – | – | 1,845 | 1,554 | 1,454 | 1,321 |

| 3 years later | – | – | – | 1,612 | 997 | 1,314 |

| 4 years later | – | – | – | – | 1,510 | 1,337 |

| 5 years later | – | – | – | – | – | 1,372 |

| Settlements | – | –182 | –150 | –121 | –121 | –208 |

| 11. Insurance business operating expenses | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Gross expenses | –1,794 | –1,786 | 0.4 |

| Reinsurers' share | 20 | 16 | 25.0 |

| Total | –1,774 | –1,770 | 0.2 |

| 12. Administrative expenses | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Staff expenses | –10,160 | –10,059 | 1.0 |

| General and administrative expenses | –6,141 | –5,904 | 4.0 |

| Depreciation/amortization and impairment losses | –933 | –932 | 0.1 |

| Total | –17,234 | –16,895 | 2.0 |

| 13. Other net operating income/expense | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Gains and losses on non-current assets classified as held for sale and disposal groups | 39 | 1 | >100.0 |

| Other operating income | 868 | 1,009 | –14.0 |

| Other operating expenses | –1,033 | –1,291 | –20.0 |

| Total | –126 | –281 | –55.2 |

| 14. Income taxes | 2015 € million | 2014 € million | Change (percent) |

|---|---|---|---|

| Current tax expense | –2,680 | –2,508 | 6.9 |

| Expense on deferred taxes | –140 | –340 | –58.8 |

| Total | –2,820 | –2,848 | –1.0 |

Current taxes in relation to the German limited companies are calculated using an effective corporation tax rate of 15.825 percent based on a corporation tax rate of 15 percent plus the solidarity surcharge. The effective rate for trade tax is 14.0 percent based on an average trade tax multiplier of 400 percent. The tax rates correspond to those for the previous year.

Deferred taxes must be calculated using tax rates expected to apply when the tax asset or liability arises. The tax rates used are therefore those that are valid or have been announced for the periods in question as at the balance sheet date.

| 2015 € million | 2014 € million | Change (percent) | |

|---|---|---|---|

| Profit before taxes | 9,787 | 10,655 | –8.1 |

| Notional rate of income tax of the Cooperative Financial Network (percent) | 29.825 | 29.825 | |

| Income taxes based on notional rate of income tax | –2,919 | –3,178 | –8.1 |

| Tax effects | 99 | 330 | –70.0 |

| Tax effects of tax-exempt income and non-tax deductible expenses | 233 | 179 | 30.2 |

| Tax effects of different tax types, different trade tax multipliers, and changes in tax rates | 5 | -1 | >100.0 |

| Tax effects of different tax rates in other countries | 15 | 8 | 87.5 |

| Current and deferred taxes relating to prior reporting periods | 56 | 166 | –66.3 |

| Reversal of valuation adjustments of deferred tax assets | 17 | 43 | –60.5 |

| Other tax effects | –227 | –65 | >100.0 |

| Income taxes | –2,820 | –2,848 | –1.0 |

The table shows a reconciliation from notional income taxes to recognized income taxes based on application of the current tax law in Germany.

D Balance sheet disclosures

| 15. Cash and cash equivalents | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Cash on hand | 6,364 | 6,409 | –0.7 |

| Balances with central banks and other government institutions | 14,171 | 9,247 | 53.2 |

| of which: with Deutsche Bundesbank | 10,921 | 6,941 | 57.3 |

| Public-sector debt instruments and bills of exchange eligible for refinancing by central banks | 1 | – | – |

| Total | 20,536 | 15,656 | 31.2 |

| 16. Loans and advances to banks and customers | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Loans and advances to banks | 32,988 | 38,293 | –13.9 |

| Repayable on demand | 17,534 | 17,331 | 1.2 |

| Other loans and advances | 15,454 | 20,962 | –26.3 |

| Mortgage loans and other loans secured by mortgages on real estate | 19 | 74 | –74.3 |

| Local authority loans | 8,577 | 10,557 | –18.8 |

| Finance leases | 100 | – | – |

| Other loans and advances | 6,758 | 10,331 | –34.6 |

| Loans and advances to customers | 700,608 | 670,683 | 4.5 |

| Mortgage loans and other loans secured by mortgages on real estate | 272,199 | 256,703 | 6.0 |

| Local authority loans | 38,091 | 41,383 | –8.0 |

| Home savings loans advanced by building society | 33,659 | 29,960 | 12.3 |

| of which: from allotment (home savings loans) | 3,651 | 4,437 | –17.7 |

| for advance and interim financing | 27,905 | 23,377 | 19.4 |

| other building loans | 2,103 | 2,146 | –2.0 |

| Finance leases | 3,575 | 4,118 | –13.2 |

| Other loans and advances | 353,084 | 338,519 | 4.3 |

| 17. Allowances for losses on loans and advances | Specific loan loss allowances € million | Portfolio loan loss allowances € million | Total € million |

|---|---|---|---|

| Balance as at Jan. 1, 2014 | 8,103 | 1,181 | 9,284 |

| Additions | 2,271 | 196 | 2,467 |

| Utilizations | –1,132 | – | –1,132 |

| Reversals | –1,824 | –305 | –2,129 |

| Other changes | 36 | –7 | 29 |

| Balance as at Dec. 31, 2014 | 7,454 | 1,065 | 8,519 |

| Additions | 2,027 | 116 | 2,143 |

| Utilizations | –984 | – | –984 |

| Reversals | –1,758 | –197 | –1,955 |

| Changes in the scope of consolidation | –14 | – | –14 |

| Other changes | –86 | 8 | –78 |

| Balance as at Dec. 31, 2015 | 6,639 | 992 | 7,631 |

| 18. Derivatives used for hedging (positive and negative fair values) | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Derivatives used for hedging (positive fair values) | 1,050 | 1,099 | –4.5 |

| for fair value hedges | 1,049 | 1,095 | –4.2 |

| for cash flow hedges | 1 | 4 | –75.0 |

| Derivatives used for hedging (negative fair values) | 9,453 | 10,423 | –9.3 |

| for fair value hedges | 9,442 | 10,395 | –9.2 |

| for cash flow hedges | 10 | 27 | –63.0 |

| for hedges of net investments in foreign operations | 1 | 1 | – |

| 19. Financial assets held for trading | Dec. 31, 2015 € million | Dec. 31, 2015 € million | Change (percent) |

|---|---|---|---|

| Derivatives (positive fair values) | 24,665 | 31,884 | –22.6 |

| Interest-linked contracts | 22,221 | 28,301 | –21.5 |

| Currency-linked contracts | 1,253 | 2,104 | –40.4 |

| Share- and index-linked contracts | 320 | 426 | –24.9 |

| Credit derivatives | 287 | 400 | –28.3 |

| Other contracts | 584 | 653 | –10.6 |

| Securities | 14,424 | 17,182 | –16.1 |

| Bonds and other fixed-income securities | 13,387 | 16,433 | –18.5 |

| Shares and other variable-yield securities | 1,037 | 749 | 38.5 |

| Loans and advances | 14,117 | 11,744 | 20.2 |

| Inventories and trade receivables | 364 | 371 | –1.9 |

| Total | 53,570 | 61,181 | –12.4 |

| 20. Investments | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Securities | 246,591 | 245,949 | 0.3 |

| Bonds and other fixed-income securities | 193,932 | 197,228 | –1.7 |

| Shares and other variable-yield securities | 52,659 | 48,721 | 8.1 |

| Investments in subsidiaries | 1,315 | 1,106 | 18.9 |

| Equity investments | 2,054 | 2,164 | –5.1 |

| Investments in joint ventures | 548 | 597 | –8.2 |

| Investments in associates | 413 | 391 | 5.6 |

| Other shareholdings | 1,093 | 1,176 | –7.1 |

| Total | 249,960 | 249,219 | 0.3 |

| 21. Investments held by insurance companies | Dec. 31, 2015 € million | Dec. 31, 2014 € million | Change (percent) |

|---|---|---|---|

| Investment property | 2,251 | 1,924 | 17.0 |

| Investments in subsidiaries, joint ventures and in associates | 527 | 504 | 4.6 |

| Mortgage loans | 8,732 | 8,047 | 8.5 |